The Great Australian Sucker Punch

When we wrote our September 2025 Portfolio Commentary, we highlighted how easing inflation had been a powerful tailwind for global asset prices. And while that remains true across much of the world as we write this commentary for the December 2025 quarter, unfortunately, the same narrative skipped Australia in the backend of 2025.

Instead of easing off the brakes, the local economy effectively slammed them on, sending growth-oriented investors straight into the windshield.

For throughout the December 2025 quarter, one theme dominated both our investment experience and the eventual performance outcome for Australian equities above all others. It was our silent, deeply frustrating companion: the relentless rise in long-term interest rates. Few forces exert a larger or more immediate influence on market valuations, and over this period it overshadowed everything else.

We illustrate this dynamic in the Australian 10 Year Bond Yield chart.

Across roughly 60 trading days, the Australian 10-year government bond yield climbed from a low near 4.10 per cent to an interim high of around 4.85 per cent by year-end, a meaningful 75-basis-point increase. On paper, that may not look dramatic, but in financial markets, moves of this magnitude in long-term rates are anything but trivial. They ripple through almost every major asset class, and growth equities, in particular, feel the force first.

At the heart of this repricing sits the same culprit that has shaped every major yield cycle for decades: INFLATION.

For a brief moment after 30 June 2025, it appeared we were out of the woods when inflation slipped neatly back into the RBA’s target band, bond yields stabilised, and markets confidently pencilled in two rate cuts for mid-2026. It was, in effect, the ideal backdrop for valuation support and your investment returns.

But the story turned on a dime. And, as we’ve noted many times, today’s markets do not hesitate when new information arrives, they move instantly. Through the back half of 2025, inflation pressures returned with real force. Annual CPI, which sat at a comfortable 1.9 per cent in June, accelerated to 3.8 per cent by October, a doubling in just a few months. Housing, services, and previously subsidised components such as electricity were responsible for much of the resurgence.

For investors, this was not a minor deviation; it was a clean break back above the RBA’s comfort zone. And once that line is crossed, the mechanics become highly consequential and inflation expectations pushed the bond market to unwind the two previously priced-in rate cuts (50bps), and instead price a 25-basis-point rate hike. In the space of a single quarter, the outlook swung from an easing cycle to a net tightening of 75 basis points. A complete reversal.

Why does this matter so much?

Because when inflation rises above the RBA’s target, investors demand higher compensation for the erosion of purchasing power over time.

That demand flows directly into higher long-term yields (as shown in the Australian 10 Year Bond Yield chart), which in particular is the anchor rate for valuing virtually all financial assets. When that anchor shifts higher, the discount rate applied to future earnings follows suit, and valuation multiples compress accordingly. Growth businesses, whose value is tied to tomorrow’s earnings rather than today’s, are naturally the most sensitive to this repricing.

What this translates into is that investors will experience the classic market phenomenon known as multiple compression. In plain terms, inflation forces a reset in the valuation lens through which future earnings are priced.

Share prices fall not because companies stumbled, but because the framework used to value them shifted.

Importantly, and this point cannot be overstated, across the entire period in question, not a single one of our portfolio companies downgraded earnings. Profitability did not deteriorate nor did the businesses themselves weaken. The adjustment happened entirely in the discounting of earnings mechanics.

You see, when long-term rates rise, the return investors require increases, and the gap between that discount rate and a company’s long-term growth rate tightens. Mathematically, that alone reduces the present value of future cash flows. You do not need to run a full discounted cash-flow model to appreciate the effect; it shows up immediately, and it shows up most acutely in companies where a larger share of value lies in future years.

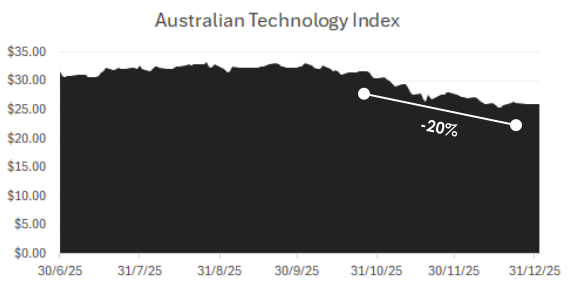

Technology shares are a prime example and the Australian Technology Industry chart shows exactly this over the same circa 60 trading days.

We are about to get a little technical, but this part matters because it explains why share prices moved the way they did.

Consider a simple illustration.

Suppose a company has a long-term growth rate of 4%, and investors require an equity risk premium of another 4%. Before the recent bond-market move, that gives you a discount rate of 8%. Introduce the 75-basis-point shift in long-term yields, and the discount rate rises to 8.75%. Nothing about the company’s earnings trajectory, strategy, or profitability has changed, only the rate used to value (or discount) those future earnings.

Small it may seem, yet mathematically, that small adjustment has an outsized effect, for a 75bps increase in

the discount rate, all else equal, reduces the valuation multiple by roughly 15–16%. That is the power of higher

long-term rates: prices fall not because businesses weaken, but because the mechanism used to convert

future growth into today’s value becomes less generous.

And when starting valuation multiples are already elevated, as they often are in technology, the effect becomes even more pronounced. A company trading on 30 times earnings can quite reasonably compress to 22–25 times purely on the back of higher discount rates. That alone translates into a 17–27% decline in price, without a single dollar of earnings changing.

In practical terms, this is simply how the mathematics of valuation works. Higher rates mechanically pull multiples lower, irrespective of whether the underlying business is performing well. It is not a commentary on quality, management, or long-term prospects. It is the unavoidable consequence of investors demanding a higher return when the risk-free rate rises.

It is an adjustment that happens across the market as a whole, and it sits entirely outside our control.

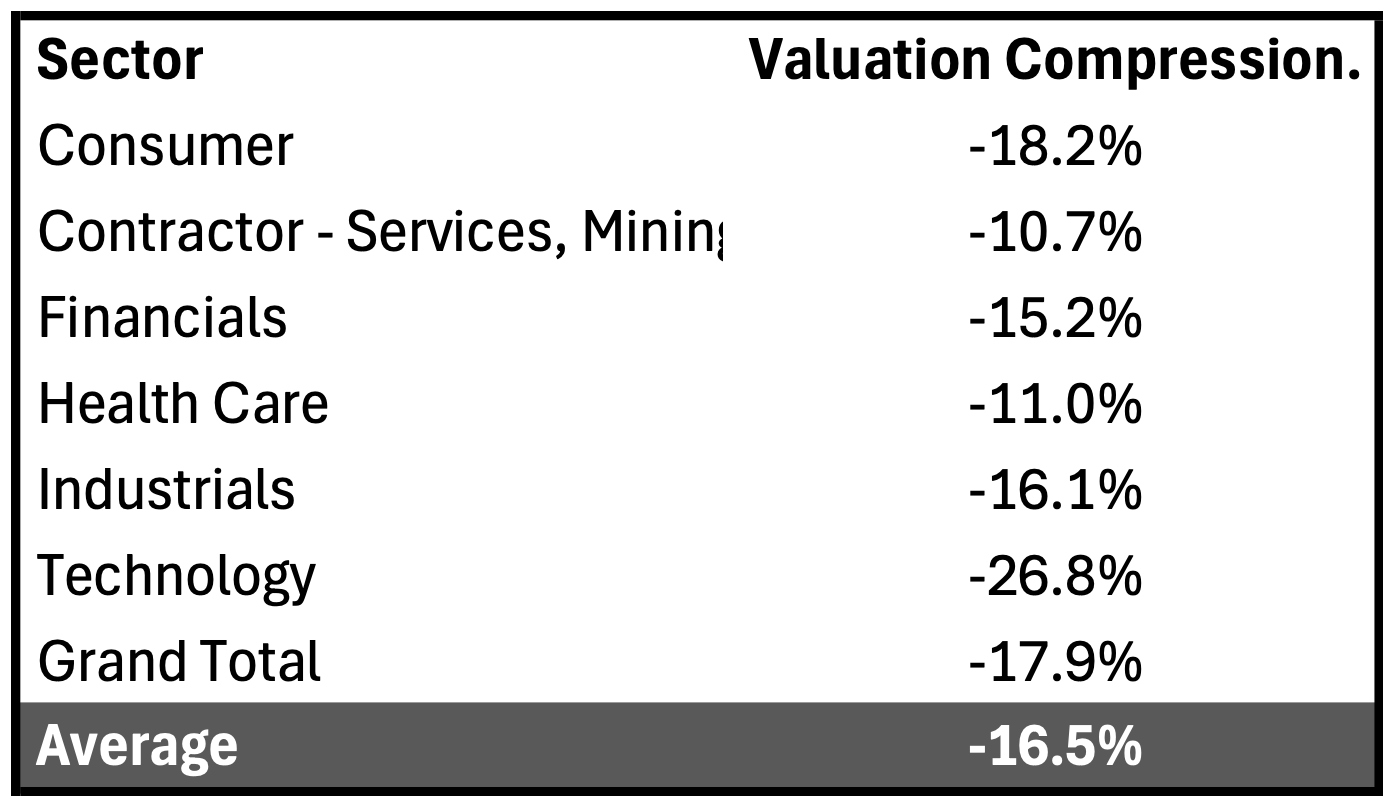

It’s precisely what has occurred in not only our Australian Equity holdings over the past three months, but over

the entire market. This is a feature we show below, with the table representing the average price falls across a

broad range of industries we follow, which include our universe of >70 companies we actively monitor.

We trust this puts all the recent moves into perspective.

Silver linings to consider

ONE

Fortunately, when you zoom out, these short, sharp valuation swings begin to fade into the background. Equity markets are full of these micro-cycles, quick bursts of volatility that feel dramatic in the moment but smooth out as time compounds. And, as we have said more times than we care to admit (ad nauseum), time remains the most powerful ally an investor has. When you stay invested in high-quality businesses with earnings that move steadily higher, the day-to-day noise of yesteryears loses relevance. The strongest growth companies, to borrow from Taylor Swift, really can “shake it off.”

Our focus therefore remains unchanged: owning businesses with durable, structural earnings growth, robust balance sheets and sensible valuations, while keeping a close eye on how long-term interest rate shifts influence the opportunity set within the portfolio(s).

It bears repeating: higher interest rates do not imply that the companies we own are weaker. They simply lift the return investors require. Prices move first. Multiples adjust. Fundamentals follow through in time, and so we continue to prioritise long-term outcomes rather than short-term fluctuations.

Patience remains essential

TWO

A second silver lining emerged just after the quarter closed. In early January, the November 2025 CPI data landed with a noticeably softer tone. Headline inflation eased to 3.4% year-on-year, down from 3.8% in October, with prices flat month-on-month. More importantly for policymakers, underlying inflation moderated as well, with the trimmed mean slipping to 3.2%. Inflation is still above the RBA’s 2–3% target range, but the immediate direction of travel appears to be slowing.

This shift possibly sets the stage for something of a reversal of what we have just endured, albeit not in full and not at the same speed. The moderation in inflation primarily potentially removes the need for the additional 25-basis-point rate rise that markets had hurriedly priced into the 10-year bond yield late last year. That repricing alone can provide meaningful relief to equity valuations, particularly across the small and mid-cap universe, where we would expect sentiment to improve as this data filters through.

It does not completely unwind the 75bps tightening shock we have just experienced, but it does help soften the edges of the micro-cycle and stabilise the valuation backdrop.

Which for Australian equities and in particular, the higher-growth segments that form our core hunting ground, this is a materially more supportive environment for investment returns if it holds true.

THREE

As we discussed in last quarter’s update, we had intentionally run with a slimmer set of direct stock positions throughout this period. Fewer positions meant less exposure to the sharpest parts of the drawdown, particularly within the model portfolios. Instead, we leaned more heavily on our core diversified exposures, which acted as an effective buffer given that large caps were largely insulated from the worst of the volatility.

By pulling back into our core settings, we were able to hold market-like performance while preserving flexibility and waiting for conditions to turn. This is another example of a recurring pattern we manage through repeatedly: build high-conviction positions when the backdrop supports it, and step back to home base when it doesn’t. These micro-cycles never disappear, they simply require discipline and a willingness to adjust, which our investment process allows for.

As you will see in the following commentary on our Australian Equities Exposure, we outline how the current phase of the cycle has created space for us to lean back into a select group of new direct positions once again.

Direct Australian Equities Exposure

As we noted earlier, the Australian market softened over the December quarter, with the ASX 200 Total Return Index down 1.01%. The contrast between sectors however was stark as we have discussed and because our exposures had already been actively managed (reduced) ahead of this, the portfolios were comparatively insulated and provided a lot of ‘dry powder’ to take advantage of the weakness.

Existing positions

AUB Group (AUB) is a very stable business yet it experienced considerable volatility through the period. In late October, Swedish private equity firm EQT submitted a takeover proposal at $45 per share, sending the stock toward $40 in November. When discussions ceased in early December, without explanation, consistent with EQT’s history of incomplete approaches, the share price fell back to around $31. Importantly, management reaffirmed guidance for net profit growth of 7.4–13.4%, so with fundamentals unchanged and the stock now trading at a meaningful discount, we increased our holding.

Zip Co (ZIP) delivered an exceptionally strong 1Q26, reporting cash EBITDA of $62.8 million, up 98% on 1Q25, driven by accelerating US momentum. US transaction volumes grew 47%, prompting management to lift FY26 US TTV guidance to above 40%. The company is also assessing a dual US listing to support its growth trajectory. We added to the position during the quarter on weakness.

ResMed (RMD) posted 9% revenue growth to $1.3 billion, alongside a 280bps margin improvement to 62%. Operating leverage supported 16% EPS growth, and cash reserves now exceed $700 million. The stock trades at its lowest P/E since the 2023 Ozempic-related sell-off, despite stable fundamentals. We continue to expect strong double-digit earnings growth through 2026 and view this as an attractive re-rating candidate.

Aussie Broadband (ABB) added ~22,600 new connections FYTD, despite price increases and NBN upgrade activity. Management reaffirmed EBITDA guidance of $157–167 million, and the stock was added to the ASX 200 in December. With solid medium-term earnings visibility, ABB remains a core position.

NEW positions

Market conditions in the December quarter presented a potential rare opportunity, the chance to buy several of Australia’s most dominant businesses at valuations we typically would not expect to see. Throughout the month, we initiated several new positions. We are hopeful that they turn out to be rewarding Christmas presents.

CAR Group (CAR), owner of Carsales.com, commands roughly 80% of online car-shopping time in Australia. The company has expanded into North America, Latin America, and Asia, evolving into a global leader. CAR s guiding for 12–14% revenue growth and 9–13% profit growth in FY26. Despite this strength, the stock has fallen 25.9% from its August highs, enabling a potentially attractive entry point.

REA Group (REA) operates Australia’s dominant property-listing platform, Realestate.com, used by 60–70% of the adult online population. August results were outstanding (revenue +15%, profit +23%), but the share price fell sharply after news that competitor Domain may be acquired by US-based CoStar. While Domain may benefit from additional investment, we believe REA’s market share and structural advantages remain intact. We purchased REA at $184, around 30% below its August highs.

Xero (XRO) is the clear leader in Australian cloud accounting software, holding an estimated 60%+ market share. Shares have been under pressure following the $3.9 billion acquisition of US payments business Melio, and while the acquisition is large, it provides the US entry point Xero has long lacked. An institutional capital raising at $183 was heavily supported by the market for the acquisition, and yet we were able to initiate our position at $115, 37% below the raise. If execution in the US succeeds, Xero could be one of the strongest earnings compounders on the ASX over the next five years.

Netwealth (NWL) is one of Australia’s fastest-growing digital wealth platforms, benefiting from a structural shift away from legacy players such as IOOF, Colonial First State, BT Panorama and AMP. While both Netwealth and Hub24 are well placed, NWL has experienced a sharper pullback, down 31.3% from August highs. We expect ongoing fund inflows to continue driving strong medium-to long-term performance.

FINAL WORDS

The volatility we saw through the December quarter, driven largely by macroeconomic forces and the sharp rise in Australian interest rates and bond yields, landed as a genuine sucker punch for parts of the market.

High-growth sectors in particular experienced what can only be described as bear-market-style multiple compression, and while uncomfortable in real time, these periods often sow the seeds for the next phase of opportunity, and that is precisely how we approached it.

Rather than retreating, we used the dislocation to selectively accumulate some of Australia’s highest-quality businesses at valuations that have not been available for quite some time. Markets rarely hand you the chance to buy dominant franchises, with recurring revenue, deep competitive moats, strong cash generation and clear multi-year growth runways, but this quarter potentially provided exactly that.

Our portfolio additions made across the period have provided all of us with exposure to market leaders, which we currently estimate will compound value for years to come. At the same time, our existing holdings continued to deliver operational resilience and earnings momentum, reinforcing our conviction in the long-term compounding characteristics of the overall portfolio.

Put simply, we were able to both fortify the foundation and lean into opportunity at the same time. A solid combination of investment fundamentals.

Taken together, we feel we are in a strong position heading into the new year: a clear strategy, high-quality businesses, and the flexibility to act decisively as conditions evolve. With half-year reporting season now only weeks away, we remain on the hunt for further opportunities that fit our framework.

Once again, thank you for your continued support and trust.

Russell Muldoon, Portfolio Manager and Bowen Hosking, Equity Analyst