TRUMP TANTRUM AND US EQUITIES

THE FALLOUT FROM TRUMP’S TANTRUM

Effectively as soon as Trump took office, a painful but important lesson played out in real time. Between March and June 2025, a fear-driven selloff triggered by tariff juiced headlines resulted in over $55 billion in global equity fund outflows. It’s not a small number, and on one of the very worst days on the 7th of April 2025, we took a screenshot of one of our individual stock and ETF watchlists, one that is largely focused on the Australian stock market. You can literally see this selling in action.

The S&P 500 plunged 12% in just four days, the VIX (a measure of stock market volatility) spiked above 45 (which is a very high reading), and panic selling ensued with our local index far from excluded.

For many investors, the volatility was reminiscent of 2008 all over again. Headlines screamed “recession,” portfolios were liquidated and cash piled up on the sidelines. The common refrain? “I’ll get back in when things calm down.”

But markets don’t wait for comfort, and by the end of June the S&P 500, Nasdaq, Russell 1000, ASX 200 and a host of other leading market price indexes had all recovered. Indeed, as I type, many of these widely followed market proxies are now recording fresh all-time highs. What was feared as being a market crash, turned out to be a test of conviction. Unfortunately, many investors failed it.

The initial pessimism surrounding tariffs turned out to be misplaced. As clarity emerged and it became clear that higher tariffs wouldn’t derail the U.S. expansion, in an economy where imports represent around 25% of consumer spending, but consumption accounts for over 70% of GDP, markets rebounded decisively especially when the Trump administration ‘pivoted’ almost overnight.

Yet those who sold in the depths of April, adopting a shoot-first, ask questions later investment approach, and who subsequently failed to reinvest, missed one of the strongest recovery windows in recent history. The opportunity cost is immense: with billions being withdrawn at the bottom and most of them missing the rally that followed (which can be seen in the data), that’s not avoiding risk, that’s locking in regret.

Let the following sink in for when we come across another period like the event(s) we have just been through: Missing just the top 10 days in the market can halve your long-term returns. And those top ays? They often come right after the worst ones. It’s worth re-reading that…

Missing just the top 10 days in the market can halve your long-term returns. And those top Days? They often come right after the worst ones.

This is why we continually stress the importance of staying fully invested. Market timing, no matter how rational it may feel in the moment, rarely works. To succeed, you must correctly call both the exit and re-entry, and most investors fail at both.

According to SPIVA®, over 90% of active managers, you know, the professional ones, the ones that do this all day, every day, some with very large teams and very smart people, underperform their benchmark over 10 years. One major reason it turns out? Market returns are often concentrated in brief, volatile periods, exactly when most people are reacting emotionally and sitting in cash.

The truth is: Long-term wealth isn’t built by flinching at every headline or soundbite. No matter how loud, or annoying and sometimes seemingly unhinged the voice is. It’s built by having a plan and sticking to it because the market doesn’t reward panic, it rewards discipline.

But don’t take my word for it, the below chart shows the main asset-allocations within your portfolios and the broad strong positive gains achieved over the 12 months (FYTD) despite everything that occurred.

For those that remained invested, the returns for the year have again been excellent. For those who didn’t… well, they need to plan better, it really is as simple as that. A center piece of such a plan could be to just take look at the most important stock index in the world, the S&P 500, and note the Annual Returns from 1928 to 2024 and just how dispersed they are.

Yet within this seemingly random series there are some hard truths:

The average return is 10% per year.

The stock market has only performed within 2% of that number in 4 of the last 97 years.

The highest annual return was +53% and the lowest was -44%.

In 71 out of 97 years, or 73% of the time, the market’s annual total return was positive.

The lesson? To get the average return, stay invested and hang on.

Australian and US Equities

Starting locally, the ASX 200 delivered a solid return of approximately 13% over the 2025 financial year, supported by improving sentiment, resilient earnings, and continued dividend strength. But in saying this, beneath the headline figure lies a growing structural trend that warrants attention, though not alarm.

For all the concerns levelled (including by us) at America’s market structure and the concentration present, particularly the dominance of mega-cap technology businesses within the S&P 500, after the year just gone it may now be Australia’s turn to take a closer look in the mirror.

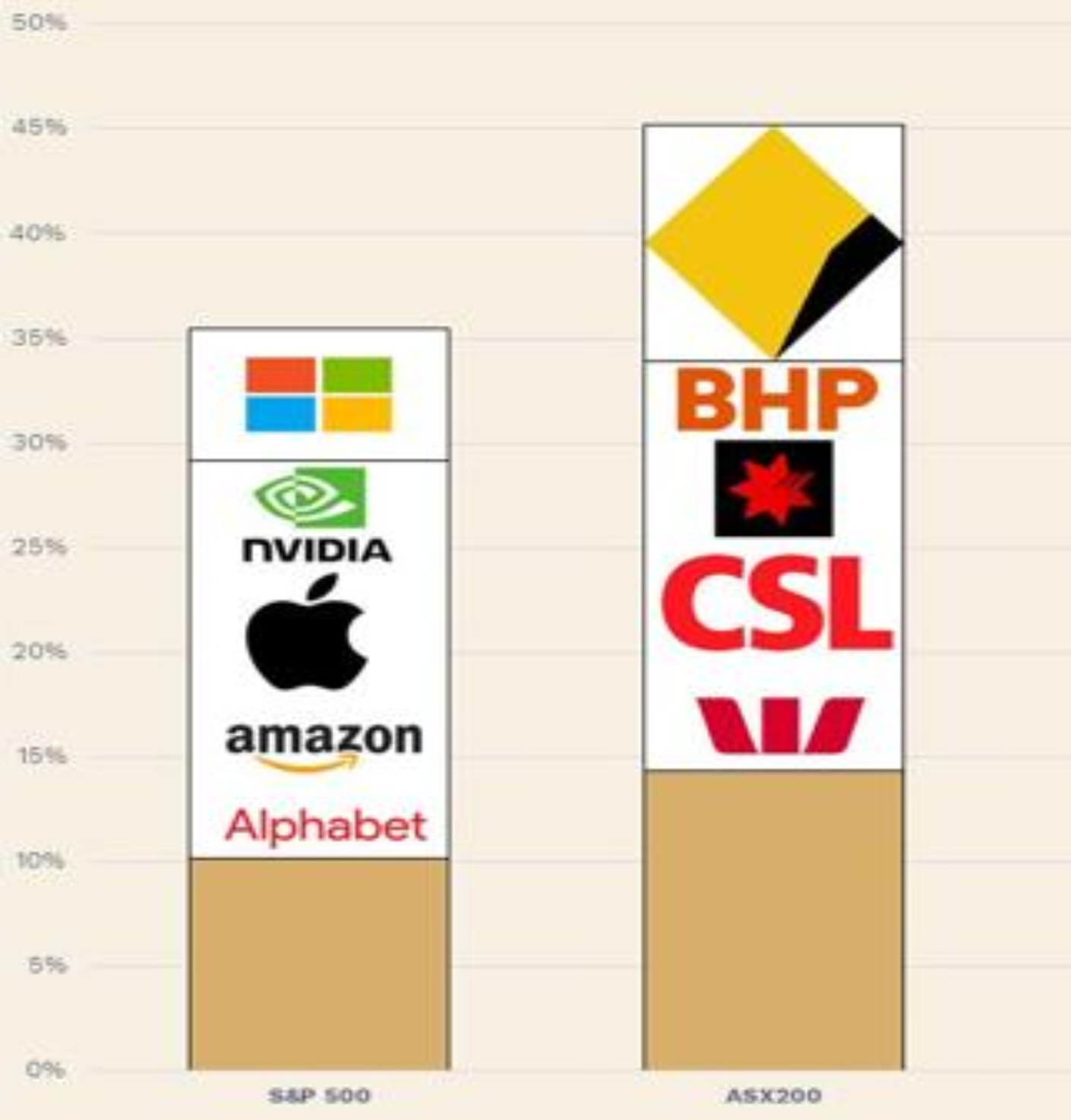

Why may you ask? Well as at mid-2025, the top 10 companies now account for nearly 50% of the ASX 200 by market capitalisation. 50%!!!

More strikingly, and just like we have seen in the US in recent periods, just a handful of names were responsible for the vast majority of the index’s return this year with CBA alone contributing 33% of the S&P/ASX 200’s total return. If we add in the other ‘Big Four’ banks plus Macquarie, just these 5 names collectively accounted for over half of the markets return.

We simply cannot recall another year quite like it - where one of the hottest stocks on the ASX in FY25 was a local bank offering a low dividend yield, anaemic earnings growth, both historical and forecast, a business that operates in a competitive, highly regulated and largely commoditised local environment and yet despite all these unflattering fundamental characteristics, it would go on to trade on the most expensive multiple of earnings that an Australian bank has traded on in the last 30 years. To add, it became and still is, the most expensive retail bank in the world… Unhinged springs to mind!

Now while we did manage to benefit from this seemingly unhinged performance through our diversified domestic exposure, it’s worth noting that despite also rising concentration in the S&P 500, we would argue it remains far more balanced by comparison. The dominant U.S. constituents are structural growth businesses embedded deeply into the global economy, companies like Apple, Microsoft, and Nvidia, underpinned by innovation, scale, and secular tailwinds. That stands in stark contrast to the Australian market’s dependence on highly valued retail banks and cyclical resource businesses, which are far more sensitive to local economic fluctuations and offer limited long-term structural growth.

From our perspective, this underscores the importance of maintaining a thoughtfully diversified portfolio, one that not only looks beyond the domestic heavyweights but also beyond Australia as an investment destination. Put simply, global diversification, both in geography and business models is essential in reducing index-specific concentration risk.

Looking Forward

If we go back and re-visit our March 2025 Quarterly report where we call out earnings growth in economies as a major driver behind each countries subsequent market performance, pleasingly the growth in 2026 looks similar to prior periods, with growth in the Nasdaq and S&P 500 still above the MSCI World average of 11.7% and Australia likely to continue languishing at the very bottom.

The clear strength of Corporate America continues to push the S&P 500 on a strong upward trajectory, hitting all-time highs and delivering solid returns through both price gains and dividend income in 2025. A picture that looks to remain intact as we head into 2026.

Sadly, we can’t say the same for Australia, where according to a recent AFR article, “More than 50pc of voters now rely on government for their main income”. Business support in our country through all the musings and promises shows no sign of immediate help from an entrenched Labor Government, with their main policy seemingly being to continue bolstering their voter base support under the guise, ‘look how we are spending money looking after you’. ‘And by the way, you better keep voting for us or it will go away’ . Is it of any wonder that above trend growth in Australia has been nonexistent for as long as we can recall?

To counteract the seemingly absence of leadership in our country, which has led to the demise of Liberal Government, who had threatened to take some of these entitlements away, we will remain active in the mid- and small-cap segments of the market which we believe may now be poised for a turnaround after a prolonged period of underperformance. With valuation dispersion between large and small caps having widened significantly, and with many quality businesses in this segment emerging from the rate-hiking cycle with cleaner balance sheets and leaner operations, coupled with interest rates expected to ease, these smaller and more dynamic businesses are more sensitive to positive inflection points, and potentially better positioned to outperform from here.

Further afield and more promisingly, the broadening of U.S. corporate earnings and market performance that we’ve been flagging for some time appears increasingly likely to play out. The narrow rally we saw early in the cycle is beginning to give way to a wider base of participation, with earnings growth extending beyond the dominant mega-caps.

In contrast to Australia where the government seems increasingly reliant on taxing a shrinking pool of businesses and non-government employed constituents, the direction of U.S. policy appears more pro-growth. The Trump Administration’s stated focus on reigniting small and medium-sized business activity speaks directly to rebuilding America’s middle class, a priority placed firmly at the top of the agenda, not the bottom.

Don’t believe us, that’s OK, but the data suggests a lot of truth here given the industrial, utilities and financial sectors have all outperformed information technology year-to-date, supported by improving forecasts for underlying earnings growth. The promise of Trump’s policy pivot to a market friendly agenda, with powerful policies like tax cuts and deregulation, just like we spoke about in a video update earlier this year, could well provide the support US-centric firms and sectors like financials and industrials need going forward.

This is very much by design, and it has taken someone truly independent of the Government system to enact what seems to be sensible long-term thinking and planning. We can all disagree on the execution (how it’s been handled and communicated) but we note this objective from the US Government and if the trend holds true, we likewise have an exposure to US Smaller Companies within your portfolios. And speaking of execution, despite us making this switch arguably too early last year, it is one we are building more confidence in as time goes on.

And sure, it would be a brave man to call the bottom here, but we do note that US Small Cap Stocks are now underperforming Mega Cap Tech Stocks by the largest margin in history. This is a story that could run for many, many years if it catches, and we are invested in the fact the start phase is likely to be soon if the US Government is successful in its initiatives.

Individual Equities Exposure

One commonly cited rule of thumb in portfolio management is that to consistently add value over time, at least 50% of your portfolio selections need to be winners. In practice, this means that for every successful pick, you're likely to have one that underperforms, an uncomfortable reality, but a reflection of just how competitive and unforgiving equity markets truly are.

The real key however is multifaceted and lies not in avoiding losses entirely (that’s impossible), but in ensuring that your winners contribute substantially more to the portfolio than your losers take away. Winning 50% of the time doesn’t mean much if your winners return 10% and your losers cost you 10%, that’s like pedalling furiously on a bike with no chain. It feels like effort, but you're not actually going anywhere.

We invest the time, hours at the desk analysing hundreds of companies, combing through thousands of numbers and management statements, not just to stay busy, but to be rewarded with meaningful, compounding gains. It’s an odd passion and pursuit, but like Lady Gaga wrote in one of her many hit songs, “Baby, I was born this way” . It is what it is…

Now, had you looked up your portfolio recently, you would have noted that you / we held eight (8) direct positions within the models up until recently. If we analyse them since our purchase dates, of those, five (5) outperformed the ASX200 Total Return index which equates to 62.5% of our holdings that ended up being winners. Remember our rule of thumb of 50%? It’s a good start. The real reward however only comes when the winners truly pull their weight, and what we’ve seen play out is that on average, while our underperformers lagged the market by 16.2% (our 3 losers), our 5 winners beat the market by 47.36% and in doing so, created a very favourable positive skew which has underpinned the portfolios strong performance over the past 3, 6, and 12 months.

Turning to the quarter just gone, our biggest winner was Zip Co (ZIP), added to the portfolio in early April. ZIP had been on our radar for some time, thanks to a remarkable turnaround under new management and a strong focus on the underpenetrated US market. When we first assessed the business, shares traded around $3.50, we could make the valuation work, but it looked fully priced for the financials we expected.

That changed as the market de-rated ZIP to a low of $1.15, despite the company delivering ~40% earnings growth in FY25 which was broadly in line with our forecasts. We waited patiently, and when management announced a share buyback, a signal even they thought their shares where cheap, this was the catalyst we needed to enter.

While we didn’t catch the absolute bottom (it bounced quickly), our initial entry at $1.50 was a comfortable start. We added at $1.68 following a strong Q3 update, and the stock continued to perform well. A guidance upgrade on June 11 further boosted momentum, with ZIP closing the quarter at $3.07—delivering a 103% return. We expect a solid August result, with FY26 guidance key to sustaining our conviction.

Location tracking app Life360 (360) was another strong performer in the June quarter, following its Q1 results. Subscription revenue grew 33%, prompting a modest upgrade to FY25 guidance. Despite the small lift, the stock surged over 20% in two days and lead us to view 360 as overvalued at current levels.

While we remain positive on Life360’s trajectory, at over $32, the asymmetry had changed, with our assessment being the risks began to outweigh the reward. As a result, we made the decision to exit the position. 360 delivered a 77% return for the quarter, and a total capital gain of over 250% from our initial purchase in February 2022 to our sale in June 2025. It of course remains on our watchlist for a more favourable pricing environment.

AUB Group (AUB) was re-rated by the market in May after upgrading FY25 guidance, expecting underlying NPAT at the upper end of the $190–$200m range. This followed a period of muted performance amid concerns over slowing premium growth. We remain confident that 4–5% premium growth is sufficient for AUB to grow earnings at 10%+ annually, supported by scale and acquisition synergies. AUB ended the quarter up 15%.

Our largest direct holding, ResMed (RMD), delivered another solid quarterly result, with revenue up 8% and net income rising 14% on margin expansion. The company continues to tap into a large, underpenetrated market, now aided and embedded by wearable devices like the Apple Watch and Garmin tracking sleep health. We expect high single-digit revenue growth and low-to-mid double- digit earnings growth, supported by cost control and manufacturing efficiencies. If this holds true, our mid-$40 per share valuation is very much achievable. RMD ended the quarter up 12.8%.

We also initiated a position in Codan (CDA) in April, based on the view that rising gold prices would boost demand for its high-margin metal detectors. Codan’s military communications segment also stands to benefit from increased global defence spending, now reaching ~5% of GDP in some regions amid heightened geopolitical tensions. CDA rose 39.4% for the quarter, and we expect a strong August result. In the January 2025 South Australian Business Index, Codan ranked 4th among all SA companies, so its also nice to be invested in one of our state’s largest employers.

We continue to hold our positions in Ansell (+1%), Aussie Broadband (+1%), and AGL Energy (–7%) and none of these companies provided material updates during the quarter. As such, their share prices largely reflected that.

While performance for these holdings was behind the broader market over the quarter, our initial purchase thesis’ remains intact. Ansell remains well-positioned as a global provider of protective solutions, Aussie Broadband continues to gain market share in the competitive telco space, and AGL is undergoing a complex but important transition toward cleaner energy generation. We expect more meaningful updates in the upcoming reporting season, which will help inform any adjustments to our positioning.

FINAL WORDS

On a personal note, my son played his 50th game of AFL football over the weekend, a proud milestone for an 11-year-old (and for his dad, too). Coincidentally, the upcoming full-year reporting season marks my own milestone in that it’s the 50th time I have gone through this process. It’s a quieter achievement, without the cheering crowds or halftime oranges, but no less meaningful.

Over the course of 25 years, I’ve come to appreciate that true skill in investing isn’t built in a single year, it’s shaped gradually, through cycles of studying businesses, listening to management teams, navigating changing macro conditions, and making decisions when the path forward isn’t always clear.

Each season brings new lessons, some reinforcing, others humbling, but all contribute to the depth of judgment and pattern recognition that only time and experience can teach. As I reflect on that, I’m reminded just how quickly time moves; some of those now entering the industry weren’t even born when this journey began, I still struggle a little to deal with that.